There is a familiar arc to how Western technology companies enter Southeast Asia. They arrive with a product that won in the United States, a playbook that worked in Europe, and the quiet assumption that the region is simply a few years behind and will eventually want what the West already has. Then they lose. Uber is the canonical example. After approximately five years, Uber sold its Southeast Asia operations to Grab in 2018, taking a minority stake in the local winner rather than trying to beat it.1 The story repeats often enough that it’s worth asking what, specifically, these imported playbooks keep getting wrong.

The mistakes are rarely about raw engineering or technology quality. They are about a set of assumptions baked so deeply into Silicon Valley product thinking, built for an entirely different economic and social infrastructure, that they remain invisible until they fail on the ground. To build successfully here, you have to unlearn the playbooks and design for the actual market realities.

Assumption 01 — The smartphone is a companion to the computer

Most Western product playbooks assume a user operates fluidly across a device ecosystem: a laptop at work, a desktop at home, and a phone in their pocket. In Southeast Asia, for hundreds of millions of people, the phone is not a companion device. It is the only device. The region leads global rankings in time spent online, mobile internet usage, and mobile app usage.2

While every global tech company knows Southeast Asia is mobile-first, fewer organizations truly internalize what that means for day-to-day engineering budgets and design choices. The operational reality is that mobile-first is practically mobile-only; the smartphone is often the only digital screen a household owns.

Operating within a mobile-only environment means managing massive hardware constraints. To maintain high daily active usage, product teams must engineer around four constant realities:

- Aggressive storage management: A minor 50MB app size increase can trigger a catastrophic drop in retention. Users will actively clear app caches or delete platforms entirely to free up phone space.

- Data cost sensitivity: Continuous, unoptimized background data usage is viewed as an unnecessary tax. Even major global tech players like Meta and Google were forced to build entirely separate, lightweight “Lite” versions of their apps specifically for emerging markets.

- Intermittent connectivity: Cellular signals regularly drop or downshift in speed outside of major urban centers.

- Hyper-local interfaces: Visual navigation must be fast, legible, and simple to understand on low-end screens.

Features that feel like minor, secondary additions on a desktop computer — resilient offline states, heavily optimized image assets, and smart background data syncing — are absolute table stakes for survival in a mobile-only market.

Assumption 02 — Everyone has a credit card

The Western growth playbook runs on frictionless card payments: enter your card once, tap to buy forever. In Southeast Asia, designing a product that requires a credit card form means excluding the vast majority of your addressable market before a single user interaction occurs.

Historically, cash dominated transactions across the region for decades, leaving millions of adults unbanked or underbanked. This infrastructure gap is precisely where imported playbooks fracture. When Uber initially launched in the region requiring payment strictly by credit card, Grab gained a massive competitive edge by building a localized network of intermediaries to help unbanked customers pay with cash.1

The product that wins isn’t the one with the most elegant checkout. It’s the one that meets people where their money actually is.

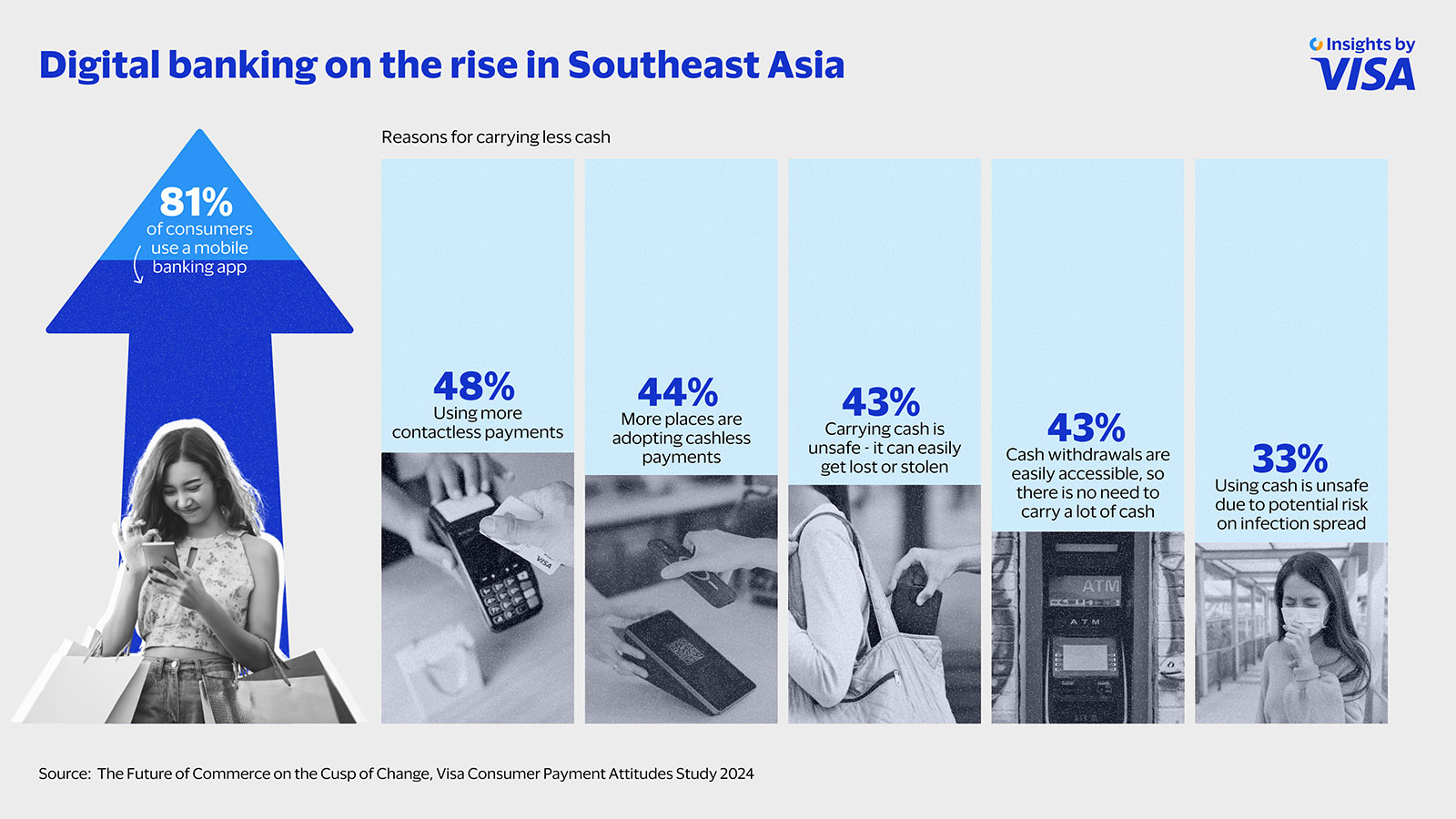

Source: Now top of mind, cashless could be top of wallets in the near future, Visa Insights 2024.

While cash remains a reality, the shift toward localized digital transactions is moving at a staggering pace, with regional digital volumes reaching roughly US$1.14 trillion.3 Instead of traditional banking infrastructure, the regional payment layer is dominated by digital wallets embedded within super-apps like GrabPay, ShopeePay, and GoPay. Users who have never owned a credit card are completely comfortable moving significant amounts of money digitally.

Digital financial inclusion in Southeast Asia is being driven almost entirely by e-wallets, embedded financial services, and national QR code standards — like VietQR in Vietnam, QRIS in Indonesia, or DuitNow in Malaysia — rather than traditional bank accounts or credit card applications.4 The transition from cash directly to mobile wallets, completely skipping the credit card phase, is a heavily researched economic phenomenon in the region.

But the lesson isn’t “cash is dying, so ignore it.” In fact, any realistic product strategy for the region must account for the persistent survival of cash on delivery (COD). Even as mobile wallet adoption accelerates, COD still commands a massive share of e-commerce transactions because it serves as the ultimate consumer guardrail against delivery-trust deficits — users want to hold the physical product in their hands before any money changes sides. Therefore, the lesson is that payment behaviour is a local, ground-level fact you have to design around, not a solved problem you can assume away.

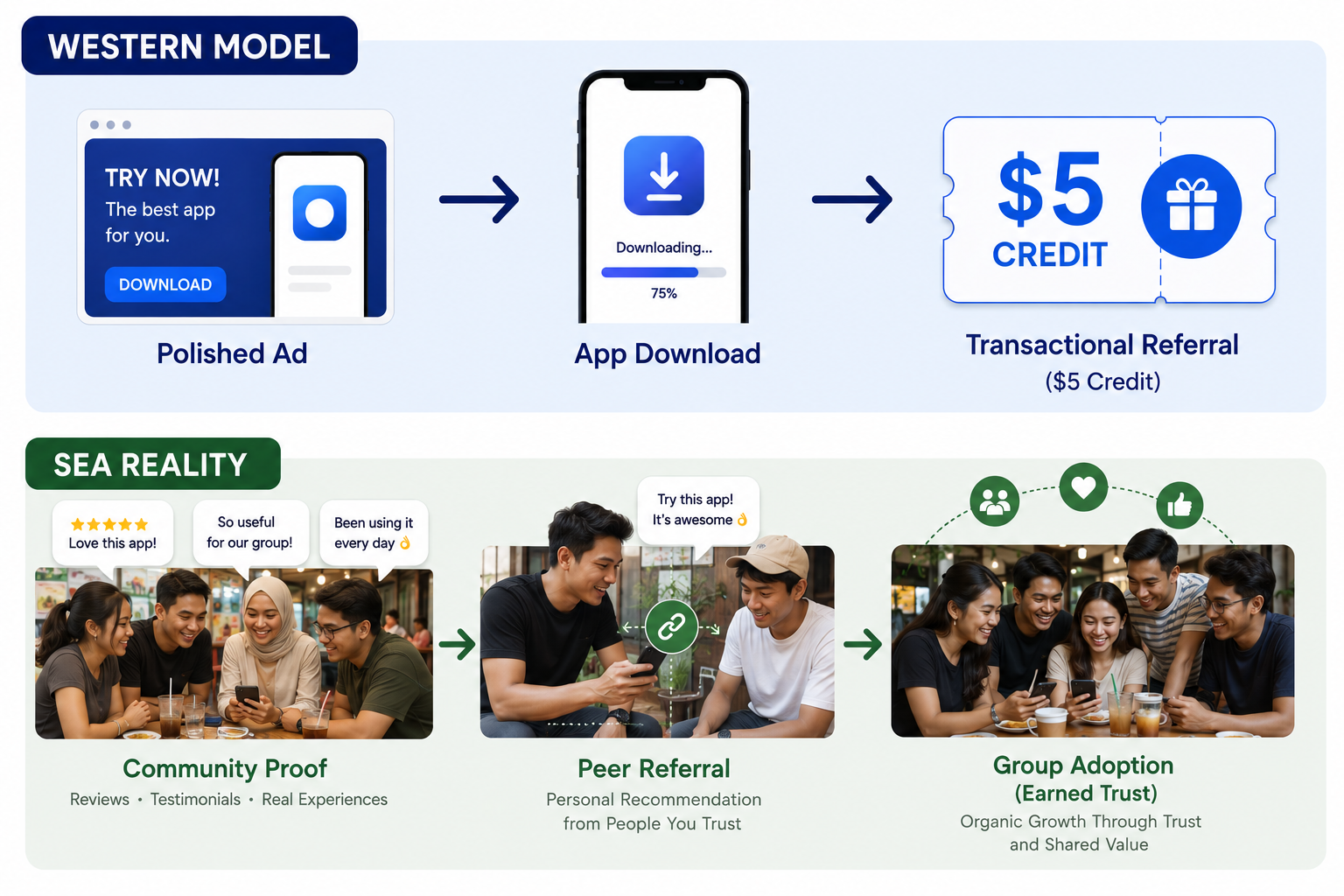

Assumption 03 — Trust is earned through strong branding

In mature Western markets, users regularly download apps from unknown software companies based on a high App Store ranking or a polished social media ad. In Southeast Asia, digital trust is earned differently. Users are inherently skeptical of platforms they haven’t vetted through their immediate personal networks.

Word of mouth isn’t just a casual growth hack here — it is the primary credibility mechanism. This completely flips how you design growth and referral loops. The classic Silicon Valley success story of Dropbox achieving explosive user growth through simple referral credits often falls flat in this region.

A digital transaction in Southeast Asia rarely happens in a vacuum. Users expect to chat with a human, ask for real-world photos, or see peer validation before hitting purchase. This is why messaging platforms like Zalo, WhatsApp, and TikTok Shop have become the dominant commerce engines in the region. They natively solve the trust deficit that standalone Western apps face.

To drive true viral adoption, referral mechanics must leverage group economics and social proof — clearly surfacing who within a user’s community is vouching for the product, turning the transaction into a shared network benefit rather than a corporate incentive.

Assumption 04 — One product, one market

A Western expansion team often treats “Southeast Asia” as a single homogenous market the way they might treat “Germany.” It is not. It is an incredibly diverse collection of eleven countries with distinct languages, regulatory bodies, religions, income levels, and localised payment rails. This fragmentation is the single most underestimated feature of the region, and it requires a deliberate structural choice:

- The deep local bet: Gojek built massive market dominance by localising relentlessly for Indonesia first, integrating deeply with local banking systems, and cementing itself as an indispensable domestic super-app before expanding.5

- The regional scale bet: Grab took the opposite path, prioritising regional presence and cross-border scalability from day one so that a user in Singapore could navigate seamlessly when landing in Vietnam.6

Both strategies are highly defensible. What isn’t defensible is ignoring the fragmentation entirely and shipping an undifferentiated, single product across the whole region. Deep localisation goes far beyond basic text translation — swapping English labels for Vietnamese, Thai, or Bahasa is a superficial baseline. True localisation requires adapting your entire product architecture to match regional habits and human behaviour.

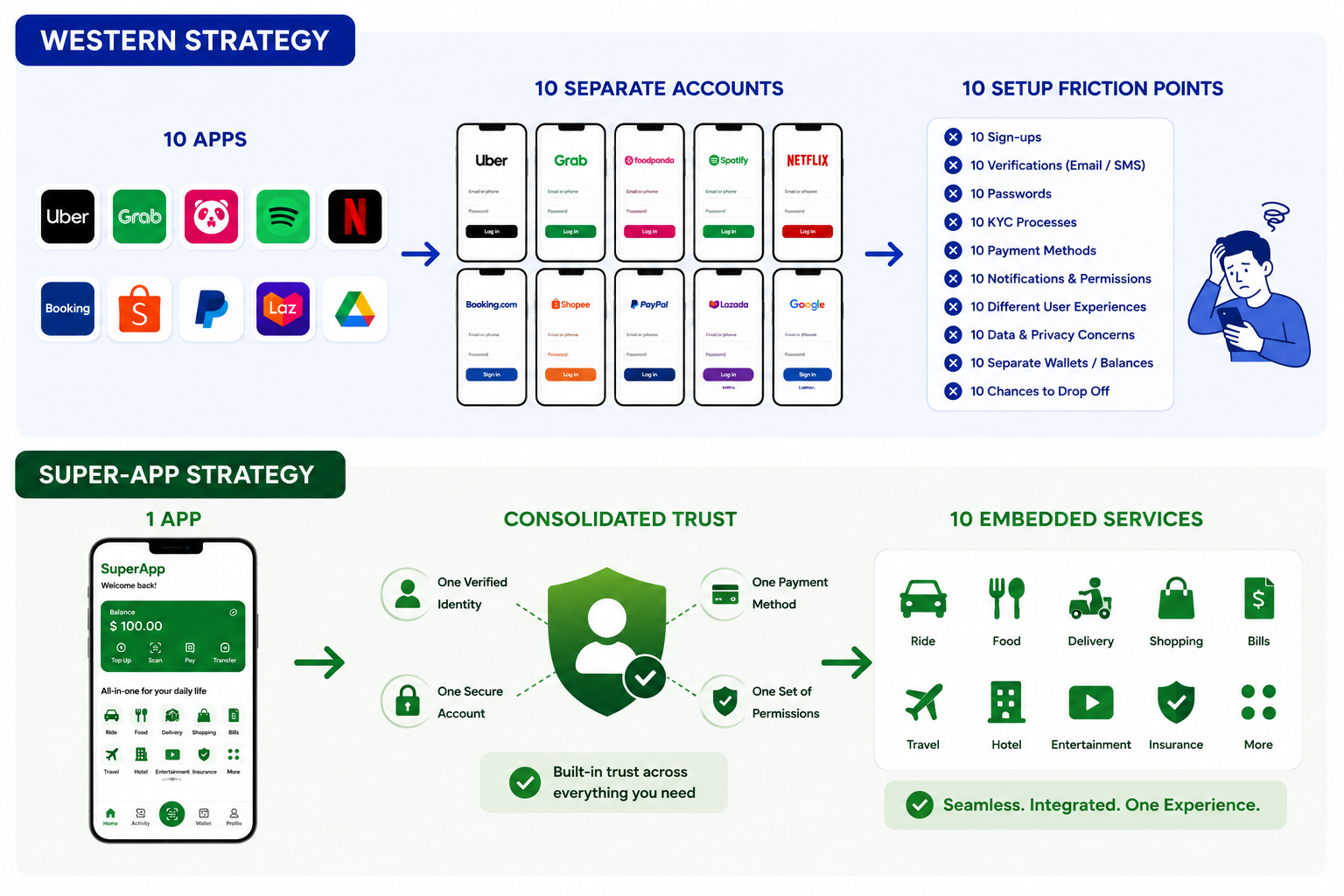

Assumption 05 — Unbundle everything

Silicon Valley orthodoxy dictates that a great product must do exactly one thing exceptionally well. In the Western playbook, bundling multiple features together is viewed as a legacy corporate habit that stifles innovation.

Southeast Asia completely inverted this rule. The region became the one place outside of China where the super-app model genuinely succeeded — all-in-one ecosystems like Grab and Gojek that offer a single unified interface for ride-hailing, food delivery, logistics, and financial services.7

Why did bundling win here? Partly because if the phone is the only device and screen space and data are precious, an app that does many things is more valuable than ten apps that each do one. Partly because trust is hard-won. Once a user trusts Grab or Gojek with their money and their daily commute, extending that trust to a new service is cheaper than a newcomer earning it from scratch. The Western instinct to unbundle reads, in this context, as a failure to understand what users actually value: convenience and trust concentrated in one place.

What the playbook should actually say

None of this means Western product thinking is useless here — rigour about metrics, user research, and iteration travels fine. What doesn’t travel is the set of buried assumptions about devices, money, trust, markets, and bundling. If I were writing the playbook for a team entering the region, it would start with five replacements:

| Product Dimensions | Western Playbook | Southeast Asian Reality |

|---|---|---|

| Hardware focus | Desktop optimization with responsive mobile viewports. | Mobile-only design. Rigid app file size limits, extreme data cost awareness, and low-bandwidth resilience. |

| Monetization | Credit-card-first billing, automated recurring subscriptions. | Wallet-first ecosystem. Instantaneous QR codes, super-app integration, and localised digital wallets. |

| Growth mechanics | Direct ad acquisition, transactional referral incentives. | Community-led growth. Social proof, peer validation, and shared network rewards. |

| Bundling strategy | Unbundle. Products must maintain a singular, highly isolated focus. | Bundle. The super-app model. Ecosystem integration is a major utility feature in a storage-constrained environment. |

| Market expansion | Treat the region as a single, uniform market block. | Fragmented strategy. Deliberate choices between deep domestic dominance or broad regional scalability. |

The Southeast Asian tech ecosystem is not behind the West; it is on an entirely different path. Because it was shaped by unique infrastructural and behavioural constraints, the region leapfrogged the West entirely — most visibly in mobile payments and super-app utility. The playbooks that fail here are the ones that mistake difference for delay. The product teams that win are the ones that start by assuming the local context knows something they don’t.